Summary Bullets:

- Revenue was down year-to-year for Ericsson, Nokia, Cisco and even ZTE, which had carried positive growth for H1 2017. But, vendors are generally doing a good job driving out costs in order to increase profitability.

- On their face, Ericsson’s Q3 2017 results reflected a company facing multiple challenges and a lengthy road to recovery. However, there were signs of light indicating that the fundamental business may return to solid footing once painful restructuring initiatives are completed.

The Bad News: Revenues Down

With the results now in for Q3 2017, it’s clear it was a rough quarter for many vendors. Results were perhaps most striking for ZTE (consolidated results shown), which experienced a nearly 8% decline compared to the prior year quarter. ZTE’s results were a distinct reversal from the first half of 2017, in which the company grew revenue 13% year-to-year.

Nokia’s Networks business results also reflected a very challenging quarter in which revenue declined by 6% on a constant currency report. Meanwhile, both Cisco (based on shipment orders) and Juniper posted revenue declines.

Ironically, for all of the attention paid to Ericsson’s continued operating struggles and restructuring pains that highlighted its Q3 2017 results, the company did report some relatively positive news: after accounting for one-time items and restructuring costs, Ericsson actually fared relatively well, with constant currency revenue declining by just 1%. Sales of network products actually increased 3% year-to-year, but were offset due to lower services sales. To be sure, Ericsson has a long way to go to extricate itself from unprofitable long-term managed services agreements; out of 42 contracts identified for renegotiation, 29 remained unresolved at the end of Q3 2017, meaning the company has much work to do before its Networks results return to profitability. Yet, there are surely signs for optimism.

REVENUE GROWTH (Q3 2017)

* Consolidated results shown. # based on y/y product orders.

* Consolidated results shown. # based on y/y product orders.

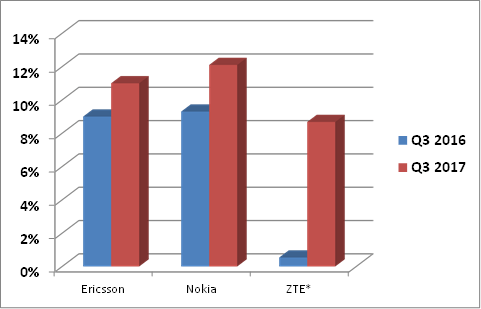

The Good News: Operating Margins Up

Despite a challenging environment for top-line growth, major vendors shown below are successfully driving costs out of the business, resulting in significant improvement in operating margin year-to-year. ZTE (again reflecting consolidated results) has gone a long way to putting itself within the ‘normal’ range for profitability compared to its closest rivals, with dramatic year-to-year improvement. Meanwhile, both Nokia and Ericsson (again accounting for one-time items that significantly impacted actual Q3 2017 reported results) showed considerable improvement year-to-year (see chart below).

“NORMALIZED” OPERATING MARGIN (Q3 2016 – Q3 2017)

* Consolidated results shown.

* Consolidated results shown.

Vendors Focusing on Profitability Despite ‘China Effect’

Early indications heading into Q4 2017 and 2018 are that many vendors are feeling the effects of a hyper-competitive environment in China as vendors attempt to position for shares in eventual 5G deals. Nokia expects competition in China to “adversely affect” Q4 2017 results; Ericsson indicated somewhat cryptically that “to position…in 5G in Mainland China, the company has managed to increase its market shares.” The translation appears to be that Ericsson offered extremely competitive pricing on its LTE gear to Chinese operators, which took its toll on gross margins, but Ericsson believes it will still be able to post double-digit operating margin in Q4 2017. Again, this does not reflect actual operating margin, which is likely to remain painfully negative due to restructuring activities and related charges that will carry into 2018. But, the company’s optimism, along with the improved results from Nokia and ZTE, does indicate that telecommunications vendors are positioning themselves to remain profitable despite the likelihood of declining operator spending and continued stiff competition.