Summary Bullets:

- AT&T and Verizon announced a joint venture with Tillman Infrastructure under which Tillman will build hundreds of cell towers across the country. Both AT&T and Verizon will lease and co-anchor towers built under the agreement.

- The deal is likely designed to pressure ‘big three’ tower companies Crown Castle, American Tower and SBA Communications to negotiate more favorable terms, but it is not clear Tillman has the clout to have much of an impact on operators’ bargaining positions.

AT&T and Verizon announced a joint venture with Tillman Infrastructure on November 13th under which Tillman will build hundreds of cell towers across the country. Both AT&T and Verizon will lease and co-anchor towers built under the agreement. The operators indicate that the deal enables them to build towers exactly where they are needed; in practice, the Tillman deal provides AT&T and Verizon with an alternative to leasing space from tower companies such as Crown Castle, American Tower and SBA Communications.

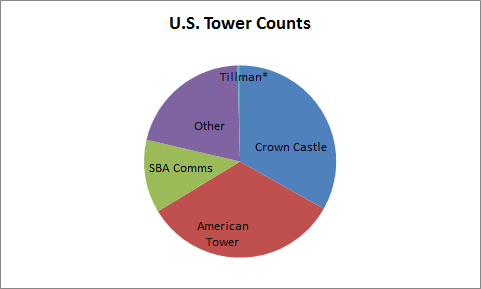

The new deal with Tillman reflects growing dissatisfaction with the current environment in the U.S. wireless market, in which operators find themselves largely at the mercy of an oligopoly of tower companies that own and lease tower space. Wireless Estimator reports that both Crown Castle and American Tower own approximately 40,000 towers, with another 15,000 owned by SBA; in total that’s almost 80% of the total U.S. tower inventory, with no other company owning more than 4,200 towers. The ‘big four’ operators have complained for the last several years that the leasing model offered by the major tower companies is increasingly untenable. Those deals typically come with ‘elevator’ arrangements in which lease rates rise modestly every year, and operators are typically charged for making changes to the equipment on the towers. As a result, all the operators have been looking to improve their bargaining positions vis-à-vis the tower companies.

As 5G looms, the need for more antennas and more radios continues to grow. Small-cell deployments potentially represent part of the solution for wireless operators by reducing demand for traditional tower sites, particularly in denser areas. Sprint in particular has hinted at a significant increase in small-cell volume coming in 2018. But small cells, despite significant focus over the past five years by both operators and vendors, still represent a tiny fraction of network coverage, and permitting and civil works ‘red tape’ are still huge obstacles to massive deployment. Recent legislative initiatives to help make it easier to deploy small cells don’t provide much hope that the regulatory challenges are going away any time soon. For example, in October, California Governor Jerry Brown vetoed a bill that would have streamlined the regulatory process by giving the state much more authority over how local governments manage small-cell applications. As a result, small cells are likely to remain a relatively small part of overall network coverage heading into the 5G era – and network operators recognize that traditional towers are and will continue to be the primary vehicle for cellular coverage.

That said, operators now find themselves in a difficult negotiating position with regard to the troika of Crown, American and SBA. (By the way, it’s worth noting that Verizon and AT&T helped create such significant market concentration by selling off lease rights to their tower portfolios to Crown and American, respectively, in the past three years.) The new alliance with Tillman seems clearly designed to pressure traditional tower operators to come up with more favorable operating terms with their operator customers. The question is whether the Tillman deal will reach a scale to have any meaningful effect on the competitive landscape.

Source: Wireless Estimator. *Assumes Tillman builds 500 towers 2018-2019.

Source: Wireless Estimator. *Assumes Tillman builds 500 towers 2018-2019.

As Tillman begins building several hundred towers in Q1 2018, it could lead to operators moving away from existing Crown, American and SBA towers. And this might have a minor effect on the large tower companies. But at least for the near term, the Tillman venture is unlikely to dramatically change the competitive dynamics between operators and towercos. Longer term, tower building is a time-consuming, capital-intensive proposition, and AT&T and Verizon have already made clear this is not a business they want to be in; as a result, they will need to find a lot more Tillmans in order to really change the competitive landscape.